What Is Auto Insurance ?

Auto insurance is a type of financial protection that provides coverage for damages or injuries resulting from a car accident. Auto insurance is mandatory in most states in the United States, with minimum coverage requirements that vary by state. However, beyond fulfilling legal requirements, auto insurance provides peace of mind for drivers, protecting them from costly expenses and liabilities in the event of an accident.

In this article, we will provide an overview of auto insurance, including the different types of coverage, the factors that affect insurance costs, and how to choose the right policy for your needs.

Types of Auto Insurance Coverage

Auto insurance policies generally provide several types of coverage, including:

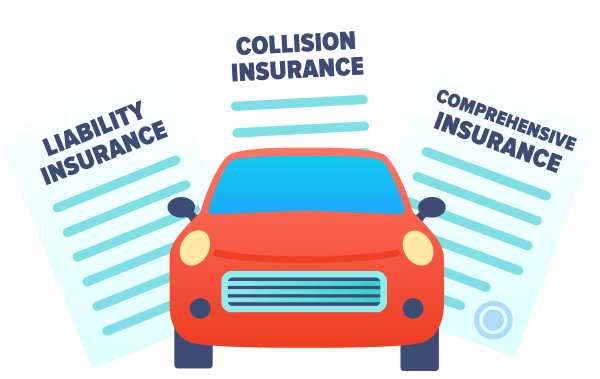

Liability Coverage

Liability coverage is the most basic type of auto insurance, and it is required in most states. This coverage pays for damages that you are legally responsible for in an accident, including injuries to other people and damage to their property. Liability coverage has two components: bodily injury liability and property damage liability.

Bodily injury liability covers medical expenses, lost wages, and other damages that result from injuries to other people in an accident that you caused. Property damage liability, on the other hand, covers damage to other people’s property, including their vehicles, buildings, and other personal property.

Collision Coverage

Collision coverage pays for damage to your vehicle in the event of an accident, regardless of who is at fault. This coverage is optional, but it is often recommended, especially for newer or more expensive vehicles.

Collision coverage typically has a deductible, which is the amount you must pay out of pocket before your insurance coverage kicks in. The higher the deductible, the lower your premiums will be, but the more you will have to pay in the event of an accident.

Comprehensive Coverage

Comprehensive coverage pays for damage to your vehicle that is not the result of a collision, such as theft, vandalism, or weather-related damage. Like collision coverage, comprehensive coverage is optional, but it can be valuable in protecting against unexpected events.

Comprehensive coverage also typically has a deductible, which can vary depending on the level of coverage you choose. Like with collision coverage, a higher deductible will result in lower premiums but higher out-of-pocket expenses in the event of a claim.

Personal Injury Protection (PIP)

Personal injury protection, or PIP, is a type of insurance that covers medical expenses and lost wages for you and your passengers in the event of an accident. PIP is required in some states, and it is optional in others.

PIP is often called “no-fault” insurance because it pays out regardless of who caused the accident. However, the amount of coverage provided by PIP can vary depending on the policy and the state in which you live.

Uninsured/Underinsured Motorist Coverage

Uninsured/underinsured motorist coverage provides protection in the event that you are in an accident with a driver who does not have insurance or who does not have enough insurance to cover your damages. This coverage is optional, but it can be valuable in protecting against the financial risk of an accident with an uninsured or underinsured driver.

Factors That Affect Auto Insurance Costs

Auto insurance premiums are determined by several factors, including:

Driving Record

Your driving record is one of the most significant factors that determine your auto insurance premiums. Drivers with a history of accidents or traffic violations are considered higher risk, and their insurance premiums will be higher as a result.

Age, Gender, and Marital Status

Younger drivers, male drivers, and unmarried drivers are statistically more likely to be involved in accidents, and their insurance premiums will reflect this increased risk.

Vehicle

The type of vehicle you drive also plays a role in determining your auto insurance premiums. More expensive or high-performance vehicles are typically more expensive to insure because they cost more to repair or replace.

Location

Where you live also affects your insurance premiums. Areas with high rates of accidents or vehicle theft are considered higher risk, and drivers in these areas can expect to pay higher premiums.

Credit Score

Your credit score can also affect your auto insurance premiums. Studies have shown that drivers with lower credit scores are more likely to file insurance claims, and as a result, they may be charged higher premiums.

Coverage and Deductibles

The amount of coverage you choose and the deductible you select also play a role in determining your insurance premiums. Higher coverage limits and lower deductibles will result in higher premiums, while lower coverage limits and higher deductibles will result in lower premiums.

How to Choose the Right Auto Insurance Policy

When choosing an auto insurance policy, it’s important to consider your specific needs and budget. Here are some tips for choosing the right policy:

Evaluate Your Coverage Needs

Consider the type of coverage you need and how much coverage you need. For example, if you have a new or expensive vehicle, you may want to consider comprehensive and collision coverage. If you live in a high-risk area, you may want to consider higher liability limits.

Compare Quotes from Multiple Providers

Shop around and compare quotes from multiple insurance providers. This will help you find the best coverage at the most affordable price.

Check for Discounts

Many insurance providers offer discounts for safe driving, bundling multiple policies, or having certain safety features on your vehicle. Check with your provider to see if you qualify for any discounts.

Read the Fine Print

Be sure to read the policy details and understand what is covered and what is not. Pay attention to any exclusions or limitations in the policy.

Consider the Provider’s Reputation

Choose a provider with a good reputation for customer service and claims handling. Read reviews and ratings from other customers to get an idea of the provider’s track record.

Conclusion

Auto insurance is a necessary expense for drivers, but it doesn’t have to be overwhelming. Understanding the different types of coverage, factors that affect insurance costs, and how to choose the right policy can help you make an informed decision and protect yourself on the road. By shopping around and comparing quotes, evaluating your coverage needs, and understanding the policy details, you can find the right auto insurance policy at the most affordable price.

Here are some frequently asked questions(Faqs) about auto insurance:–

1 – What is auto insurance?

Auto insurance is a type of insurance policy that provides financial protection for drivers in the event of an accident or other covered event, such as theft or vandalism. It can help cover the costs of repairs or replacement of a damaged vehicle, medical expenses for injuries sustained in an accident, and other related expenses.

2 – Is auto insurance required by law?

Yes, in most states, auto insurance is required by law. The specific requirements vary by state, but typically drivers are required to have liability insurance, which covers damages or injuries that the driver may cause to others.

3 – What are the different types of auto insurance?

The most common types of auto insurance include liability insurance, collision insurance, comprehensive insurance, and personal injury protection. Liability insurance covers damages or injuries that you may cause to others, while collision insurance covers damages to your own vehicle in the event of a collision. Comprehensive insurance covers damages or losses caused by events such as theft, fire, or natural disasters, and personal injury protection provides coverage for medical expenses and other related expenses resulting from an accident.

4 – How are auto insurance premiums calculated?

Auto insurance premiums are calculated based on a variety of factors, including the driver’s age, driving record, location, type of vehicle, and coverage limits. Insurance providers use complex algorithms and risk models to determine the likelihood of a driver filing a claim and the potential cost of that claim, and they adjust premiums accordingly.

5 – How can I save money on auto insurance?

There are several ways to save money on auto insurance, including:

- Choosing a higher deductible

- Bundling multiple policies with the same provider

- Maintaining a good driving record

- Taking advantage of discounts offered by your provider

- Shopping around and comparing quotes from multiple providers

Note – This blog is Just for information Purpose. Before investing and taking any kind of financial decision, please consult with your financial advisor , Read the company policies carefully, Interest rates, Time duration and many more …